https://www.batonrougerealestateappraisal.com// – Why Did RE Agent Send Appraiser 5 and 6 Year Old Homes As Comps For 20 Year Old Subject?

The longer I appraise homes for purchases, the less I understand about how homes are properly and ethically priced for listings! This post is about an example in the Greater Baton Rouge housing market I recently experienced. THE HOME DID NOT APPRAISE FOR THE PURCHASE PRICE! AND, this was one of those deals where they tried to roll in excessive seller paid concessions.

The longer I appraise homes for purchases, the less I understand about how homes are properly and ethically priced for listings! This post is about an example in the Greater Baton Rouge housing market I recently experienced. THE HOME DID NOT APPRAISE FOR THE PURCHASE PRICE! AND, this was one of those deals where they tried to roll in excessive seller paid concessions.

Disclaimer. In order to protect the identity of the Agent and the home in question, which is still Pending, details as to location and physical address are withheld.

Physical Details. Subject or home under contract is located somewhere in Greater Baton Rouge. Subject is 20 years old, 1,750sf to 2,000sf 3 bedrooms, 2 bathrooms located in a restricted subdivision where the homes are similar size and age. There is 1 sale and current listings in this development. Price range is somewhere between $180,000 to $220,000. While subject is in good condition, it’s not updated and has some inferior vinyl flooring.

Appraisal Inspection Setup & Request For Comps Used To Market Subject. As is my custom, at the same time the appraisal inspection was setup, the comps used to market the home were requested from Listing Agent. I’ve always believed that there are 2 to 3 real estate professionals involved in the sale or purchase of a home: the Listing Agent, Selling Agent and The Appraiser. Agents do know and see things in the market that appraisers do not and I want to know what I might be missing about a deal. School district could be an example. And, by requesting the comps up front, I hope to avoid an appeal or rebuttal later.

Home Was Priced High And The Sellers Gave it Away! Before visiting subject, I noticed subject was priced high and Agent provided 5 “sales”, which turned out NOT to be true comps. When I arrived at the home, the sellers were obviously nervous and were asking me questions about the appraisal and comps and making stating statements like, “I hope the home appraises with the extra concessions rolled in because we have a contract on another home…..”

The “Sales”, not “Comps” Sent. Also, Note That Appraisal Is Being Completed In March 2011 and Lenders Want Comps Within 90 to 180 Days Or 3 to 6 Months. Here’s a review of the 5 sales sent to me.

Sale #1, sold in 4/2010, is 200sf smaller in size, is similar in age but is updated. While this sale can be added a supplemental comp, this “sale” is too old for underwriters in 2011 to give heavy consideration to it.

Sale #1, sold in 4/2010, is 200sf smaller in size, is similar in age but is updated. While this sale can be added a supplemental comp, this “sale” is too old for underwriters in 2011 to give heavy consideration to it.

Sale #2, sold in 6/2010, is 240sf smaller in size, was built in 2006 or is 5 years old, is located in a newer development with a newer design/appeal. So, design/appeal, age, location and condition are all superior. How is this “5” year old home comparable to a 20 year old home? The 240sf difference in size raises the gross and net adjustments above underwriter tolerance of 15%, which indicates it’s not truly a comparable. Also, the 6/2010 “sale” is too old for underwriters in 2011 to give heavy consideration to it. I couldn’t believe what I was seeing here!

Sale #3, sold in 8/2010, is 312sf smaller in size, was built in 2005 or is 6 years old, is located in a newer development with a newer design/appeal AND an IG Pool. So, design/appeal, age, SLAB GRANITE COUNTERS, location, IG Pool and condition are all superior. How is this “6” year old home comparable to a 20 year old home? The 312sf difference in size raises the gross and net adjustments above underwriter tolerance of 15%, which indicates it’s not truly a comparable. Also, the 8/2010 “sale” is too old for underwriters in 2011 to give heavy consideration to it. I couldn’t believe what I was seeing here!

Sale #4, sold in 10/2010 is within 75sf of subjects size, BUT was built in 2000 or is 11 years old, has a newer design/appeal AND is located on a half acre subdivision lot. So, design/appeal, age lot size and condition are all superior. How is this “11” year old home comparable to a 20 year old home?

Sale #5, sold in 6/2010, is within 75sf of subjects size, is similar in age and condition. While this sale can be added a supplemental comp, this “sale” is too old for underwriters in 2011 to give heavy consideration to it.

What I did and didn’t do! This appraiser ended up using Sales 1, 4 & 5 in the report, Sale 4 simply because of the lack of sold homes in this market, along with 2 other more recent solds to comply with underwriters wanting more recent comps. This appraiser did not bend ethics and use Sales 2 & 3 as there was NO remote similarity to the subject and 5 & 6 year old homes. And, per lender requirements, this appraiser also added 3 listings into the report from the immediate market, of which were located in subjects own development.

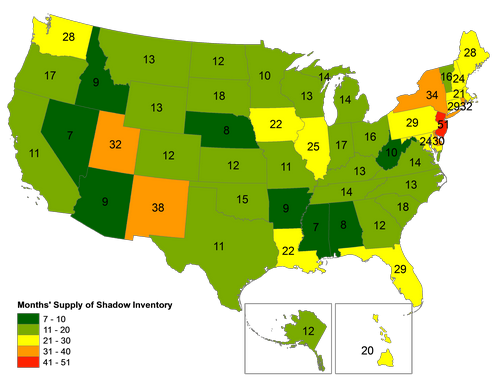

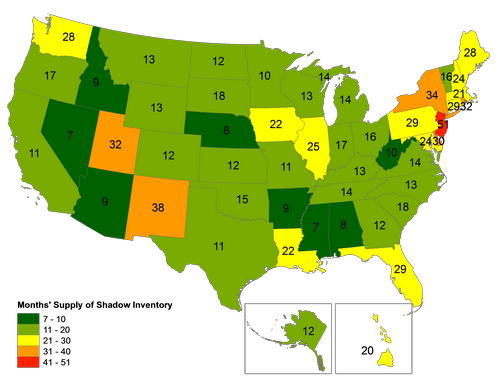

THIS IS NOT A HOUSING MARKET OF STRENGTH AND….THIS POST HURRICANE KATRINA MARKET IS UNDERSTANDABLY AND LOGICALLY STILL CORRECTING! While GBR is performing better than the general U.S. housing market, we do face challenges. There has been a barrage of economic data and news suggesting national economic malaise in the housing sector with no signs whatever of even price footing, U.S. home prices continue to fall, and Corelogic and Baton Rouge Business Report reporting that Greater Baton Rouge is in its’ 6TH STRAIGHT MONTH OF HOME PRICE DECLINES. Greater Baton Rouge also has a fore closure and shadow inventory problem with 22 months of current shadow inventory. I’m not here to put down our market, but I do believe it’s about time we admit the challenges and price local listings accordingly, especially in the under $300K range where it really matters. The over $300,000 market appears to be weathering this downturn better than the under $300,000 markets.

WHAT I DON’T SOMETIMES SEE IN THE GBR HOUSING MARKET. What I don’t see sometimes, not all the time, are GBR home listings priced according to these facts and trends above! Some homes are priced as if it were still 2007. Homes shouldn’t be listed based on the sellers dictating listing price but rather based on market support and a little cushion for negotiation and normal seller concessions.

LOW APPRAISALS. And, when homes are overpriced, this is why that “low appraisal” occurs. Low Appraisals could be the result of a faulty appraisal, and/or it could be more about bringing reality to the situation and reflecting a flaw in the expectations created by a faulty and unrealistic listing pricing at the beginning of the process. This is exactly the example I have provided in this article, the totally unrealistic listing price for this home that didn’t appraise. And, it didn’t appraise based on the Agent’s 3 actual comps and the 1 sale and 2 current listings in the subjects own development. I believe those 5 & 6 year old “sales” provided were to help prop up the deal, which didn’t happen with this appraiser!

REASONS FOR LOW APPRAISALS. Low Appraisals can occur because the home listed wasn’t actually measured…this does happen in our market. Low appraisals can occur because the listing agents failed to deduct excessive seller paid concessions when they completed that MLS CMA to price that home. And, the GBRMLS doesn’t automatically deduct excessive concessions. So, if local agents don’t do more than a simple MLS CMA to price their listings, if they don’t examine seller paid concessions on each sale they base value, they could end up with a low appraisal because that appraiser IS going to deduct excessive seller paid concessions on comps used based on Fannie Mae selling guidelines, which instructs appraisers to do so below:

“Lenders are reminded that excessive sales concessions can artificially inflate the sales price of a property, which can then lead to an inflated market value. Particular attention should be given to unusual sales or financing concessions to ensure that they are properly accounted for in the appraisal report. Fannie Mae’s definition of market value is intended to ensure that appraisals reflect an opinion of market value after adjustments for any special or creative financing or sales

concessions have been made, such as interest rate buydowns or payment of condo or homeowners’ association fees.”

Fannie Mae and FHA know that when there’s no skin-in-the-game or down payment, there could be a higher default rate!

GREATER BATON ROUGE HOME BUYERS SHOULD GET A PRE-PURCHASE HOME APPRAISAL! With the local housing market still correcting and “some” overpriced listings in this market, it’s this appraisers advice to get a Pre-Purchase Home Appraisal before negotiations!

GREATER BATON ROUGE HOME BUYERS SHOULD GET A PRE-PURCHASE HOME APPRAISAL! With the local housing market still correcting and “some” overpriced listings in this market, it’s this appraisers advice to get a Pre-Purchase Home Appraisal before negotiations!